Delaying retirement savings is a critical error that can significantly jeopardize your financial future, according to personal finance expert Suze Orman. Orman stresses that starting early, even with small contributions, is crucial due to the power of compounding interest, warning that procrastination can lead to substantial financial shortfalls in later years.

Suze Orman, the renowned personal finance guru, is issuing a stark warning to individuals of all ages: putting off saving for retirement is a “huge money mistake” that must be avoided at all costs. In an era defined by financial uncertainties and fluctuating market conditions, Orman’s advice serves as a critical reminder of the importance of long-term financial planning and the detrimental consequences of procrastination. Her core message revolves around the unparalleled power of compound interest and the irreplaceable advantage of starting early, regardless of the initial contribution size.

Orman’s perspective is rooted in the fundamental principle that time is the most valuable asset when it comes to investing. Compound interest, often described as the “eighth wonder of the world,” allows your earnings to generate further earnings, creating a snowball effect that can dramatically increase your wealth over time. By delaying the start of your retirement savings, you not only miss out on the potential growth of your initial investments but also sacrifice years of compounded returns that could significantly bolster your financial security in retirement.

“The biggest mistake people make is thinking they have plenty of time to start saving for retirement,” Orman cautions. “Every year you delay, you’re not just missing out on contributions; you’re missing out on the potential growth of those contributions. Time is your greatest ally in investing, and you can’t get it back once it’s gone.”

To illustrate the point, Orman often uses hypothetical scenarios to demonstrate the impact of starting early versus starting late. For example, consider two individuals: Sarah, who begins investing $200 per month at age 25, and John, who waits until age 35 to start investing the same amount. Assuming an average annual return of 7%, Sarah would have accumulated significantly more wealth by the time she reaches retirement age, simply because she started earlier and allowed her investments more time to grow. The difference in their final balances could be tens or even hundreds of thousands of dollars, highlighting the profound impact of early investing.

Orman’s advice is particularly relevant in today’s economic climate, where factors such as inflation, rising healthcare costs, and longer life expectancies are placing increasing pressure on retirement savings. With traditional pension plans becoming less common, individuals are increasingly responsible for managing their own retirement funds, making it even more critical to start early and save diligently.

Moreover, Orman emphasizes that it’s never too late to start saving, even if you’ve already delayed. While starting early provides the greatest advantage, any amount of savings is better than none. She encourages individuals to assess their current financial situation, create a budget, and identify opportunities to cut expenses and allocate more funds towards retirement savings.

One of the key aspects of Orman’s financial philosophy is the importance of financial literacy and empowering individuals to take control of their financial futures. She advocates for educating yourself about investment options, understanding the risks and rewards, and seeking professional advice when needed.

The Power of Compounding and Early Investment

The cornerstone of Orman’s argument lies in the concept of compounding interest, a financial phenomenon where the interest earned on an investment also earns interest. This exponential growth can significantly amplify returns over time, making early investment particularly advantageous. To truly understand the power of compounding, it’s essential to delve deeper into its mechanics and explore how it can transform modest savings into substantial wealth.

Compounding works by reinvesting the earnings generated by an investment, allowing them to generate further earnings. This creates a snowball effect, where the principal amount grows at an accelerating rate. The longer the investment horizon, the greater the impact of compounding.

Consider a simple example: if you invest $1,000 in an account that earns 7% interest per year, you would earn $70 in interest after the first year. In the second year, you would earn interest not only on the original $1,000 but also on the $70 in interest from the first year. This means you would earn slightly more than $70 in the second year, and the amount would continue to increase each year as the interest compounds.

The formula for calculating compound interest is:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

To illustrate the difference between starting early and starting late, let’s compare two scenarios:

Scenario 1: Sarah starts investing $200 per month at age 25, earning an average annual return of 7%.

Scenario 2: John starts investing $200 per month at age 35, earning the same average annual return of 7%.

By the time both individuals reach age 65, Sarah would have invested a total of $96,000 ($200 per month for 40 years), while John would have invested a total of $72,000 ($200 per month for 30 years). However, due to the power of compounding, Sarah’s investment would have grown to approximately $497,000, while John’s investment would have grown to approximately $226,000.

The difference of $271,000 highlights the significant advantage of starting early. Even though Sarah invested only $24,000 more than John, her investment grew much more substantially due to the additional 10 years of compounding.

Beyond the Numbers: Psychological and Behavioral Factors

While the mathematical benefits of early investment are undeniable, there are also important psychological and behavioral factors that contribute to the importance of starting early. Developing good saving habits early in life can set the stage for long-term financial success, while procrastination can lead to feelings of anxiety and regret.

One of the biggest challenges in saving for retirement is overcoming the temptation to prioritize immediate gratification over long-term financial security. Many people struggle to delay spending money on non-essential items, even when they know they should be saving for retirement. This is where the concept of “paying yourself first” comes into play.

“Paying yourself first” means making saving a priority, rather than an afterthought. It involves setting aside a portion of your income for savings and investments before you pay your bills or spend money on discretionary items. By automating your savings and making it a regular habit, you can overcome the temptation to spend that money on something else.

Another psychological factor that can hinder retirement savings is the tendency to underestimate the amount of money needed to maintain a comfortable standard of living in retirement. Many people assume that their expenses will decrease significantly in retirement, but this is not always the case. Healthcare costs, travel expenses, and other unexpected costs can quickly deplete retirement savings.

Therefore, it’s essential to create a realistic retirement plan that takes into account all potential expenses. This plan should include a detailed budget, an estimate of your future income needs, and a strategy for managing your investments.

Strategies for Overcoming the Procrastination Hurdle

Orman offers several practical strategies for individuals who are struggling to overcome the procrastination hurdle and start saving for retirement:

- Start Small: Don’t feel like you need to make large contributions to start. Even small amounts can make a big difference over time, thanks to the power of compounding. “Start with whatever you can afford, even if it’s just $25 or $50 per month,” Orman advises. “The important thing is to get started and build momentum.”

- Automate Your Savings: Set up automatic transfers from your checking account to your retirement account each month. This will make saving effortless and ensure that you consistently contribute to your retirement fund. Most employers offer automatic payroll deductions for 401(k) plans, making it easy to save directly from your paycheck.

- Take Advantage of Employer Matching: If your employer offers a 401(k) match, be sure to take full advantage of it. This is essentially free money, and it can significantly boost your retirement savings. For example, if your employer matches 50% of your contributions up to 6% of your salary, you should contribute at least 6% of your salary to your 401(k) to receive the full match.

- Reduce Expenses: Identify areas where you can cut back on spending and redirect those funds towards retirement savings. This could involve reducing your entertainment expenses, eating out less often, or finding ways to save on transportation costs. Even small changes can add up over time.

- Seek Professional Advice: If you’re feeling overwhelmed or unsure about how to start saving for retirement, consider seeking advice from a qualified financial advisor. A financial advisor can help you assess your financial situation, create a retirement plan, and choose appropriate investments.

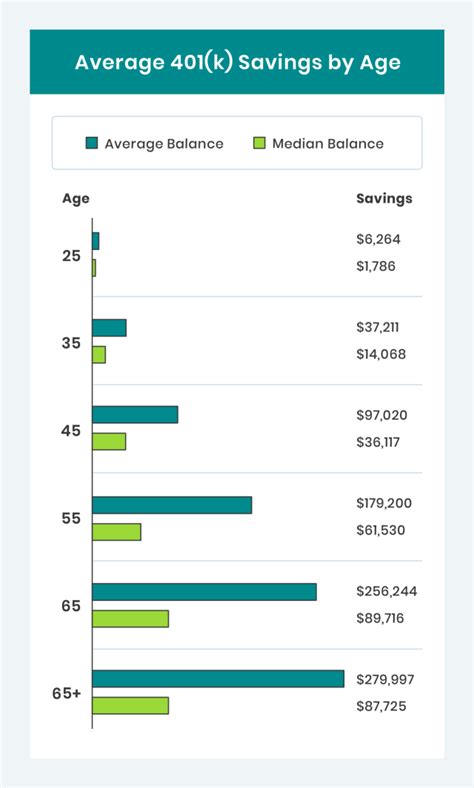

Retirement Accounts: 401(k)s and IRAs

Orman frequently emphasizes the importance of utilizing tax-advantaged retirement accounts, such as 401(k)s and Individual Retirement Accounts (IRAs), to maximize savings potential. These accounts offer significant tax benefits that can help your money grow faster and provide more financial security in retirement.

A 401(k) is a retirement savings plan offered by many employers. It allows employees to contribute a portion of their pre-tax salary to a retirement account, and the contributions are often matched by the employer. The money in a 401(k) grows tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw them in retirement.

An IRA is a retirement savings account that individuals can open on their own, regardless of whether they have access to a 401(k) through their employer. There are two main types of IRAs: Traditional IRAs and Roth IRAs.

Traditional IRAs offer tax-deductible contributions, meaning you can deduct the amount you contribute from your taxable income in the year you make the contribution. The money in a Traditional IRA grows tax-deferred, and you pay taxes on the withdrawals in retirement.

Roth IRAs offer no upfront tax deduction, but the money in a Roth IRA grows tax-free, and withdrawals in retirement are also tax-free. This can be a significant advantage for individuals who expect to be in a higher tax bracket in retirement.

Orman generally recommends contributing to a Roth IRA if you are eligible and expect to be in a higher tax bracket in retirement. If you are not eligible for a Roth IRA or expect to be in a lower tax bracket in retirement, a Traditional IRA may be a better option.

Investing Strategies for Retirement Savings

Once you’ve opened a retirement account, the next step is to choose appropriate investments. Orman advises diversifying your investments across different asset classes, such as stocks, bonds, and real estate, to reduce risk and maximize potential returns.

Stocks are generally considered to be riskier than bonds, but they also have the potential to generate higher returns over the long term. Bonds are generally considered to be less risky than stocks, but they also tend to offer lower returns. Real estate can provide diversification and potential appreciation, but it also involves higher transaction costs and illiquidity.

Orman recommends investing in a mix of stocks and bonds that is appropriate for your age, risk tolerance, and investment goals. As a general rule, younger investors with a longer time horizon can afford to take on more risk by investing a larger percentage of their portfolio in stocks. Older investors with a shorter time horizon may want to reduce their risk by investing a larger percentage of their portfolio in bonds.

Addressing Common Concerns and Misconceptions

Many people have concerns and misconceptions about saving for retirement that can prevent them from taking action. Orman addresses some of the most common concerns and offers practical solutions.

- “I can’t afford to save for retirement.” Orman emphasizes that even small amounts can make a big difference over time. She encourages people to start with whatever they can afford and gradually increase their contributions as their income grows. She also suggests looking for ways to cut expenses and redirect those funds towards retirement savings.

- “I’ll start saving when I’m older and have more money.” Orman warns that delaying retirement savings can be a costly mistake. The longer you wait, the more you’ll need to save each month to reach your retirement goals. She emphasizes the importance of starting early, even with small contributions, to take advantage of the power of compounding.

- “I don’t know anything about investing.” Orman encourages people to educate themselves about investment options and seek professional advice when needed. She recommends reading books, attending seminars, and consulting with a qualified financial advisor. She also suggests starting with simple, low-cost investment options, such as index funds and exchange-traded funds (ETFs).

- “I’m too old to start saving for retirement.” Orman emphasizes that it’s never too late to start saving. While starting early provides the greatest advantage, any amount of savings is better than none. She encourages people to assess their current financial situation, create a retirement plan, and start saving as much as they can afford.

- “Social Security will be enough to cover my retirement expenses.” Orman cautions that Social Security is not designed to be the sole source of retirement income. It’s important to supplement Social Security with personal savings and investments to ensure a comfortable retirement.

Beyond Retirement Savings: Holistic Financial Planning

While retirement savings is a critical component of financial planning, Orman emphasizes the importance of taking a holistic approach to managing your finances. This includes managing debt, building an emergency fund, protecting your assets with insurance, and creating a will or trust.

Managing debt is essential for achieving financial security. Orman recommends paying off high-interest debt, such as credit card debt, as quickly as possible. She also advises avoiding taking on unnecessary debt and living within your means.

Building an emergency fund is crucial for protecting yourself against unexpected expenses, such as job loss or medical bills. Orman recommends having at least six to eight months’ worth of living expenses in a readily accessible savings account.

Protecting your assets with insurance is important for mitigating financial risks. Orman recommends having adequate health insurance, life insurance, disability insurance, and homeowner’s or renter’s insurance.

Creating a will or trust is essential for ensuring that your assets are distributed according to your wishes after your death. Orman recommends consulting with an estate planning attorney to create a comprehensive estate plan.

Conclusion: Taking Control of Your Financial Future

Suze Orman’s warning about delaying retirement savings serves as a powerful reminder of the importance of long-term financial planning and the detrimental consequences of procrastination. By starting early, even with small contributions, you can harness the power of compounding interest and build a secure financial future. Remember that it is never too late to start, and seeking professional advice is a smart move to make the right financial decisions. It’s crucial to overcome psychological barriers, develop good saving habits, and take advantage of tax-advantaged retirement accounts. By taking control of your finances and making informed decisions, you can achieve financial freedom and enjoy a comfortable retirement.

Frequently Asked Questions (FAQ)

-

What is the biggest money mistake people make regarding retirement, according to Suze Orman? According to Suze Orman, the biggest money mistake people make is delaying saving for retirement. She emphasizes that starting early, even with small contributions, is crucial due to the power of compounding interest.

-

Why does Suze Orman emphasize the importance of starting to save early for retirement? Orman emphasizes starting early because of the power of compound interest. The earlier you start, the more time your money has to grow exponentially, leading to a significantly larger nest egg by retirement. Starting early also allows you to make smaller contributions over a longer period, rather than needing to save larger amounts later in life.

-

What does Suze Orman recommend for those who feel they cannot afford to save much for retirement right now? Orman recommends starting with whatever you can afford, even if it’s a small amount like $25 or $50 per month. The key is to get started and build momentum. She also suggests automating savings and looking for ways to cut expenses to redirect funds toward retirement.

-

What types of retirement accounts does Suze Orman often recommend? Orman frequently recommends utilizing tax-advantaged retirement accounts such as 401(k)s and Individual Retirement Accounts (IRAs). She often advises contributing to a Roth IRA if you are eligible and expect to be in a higher tax bracket in retirement.

-

Besides retirement savings, what other aspects of financial planning does Suze Orman emphasize? Beyond retirement savings, Orman emphasizes holistic financial planning, which includes managing debt, building an emergency fund, protecting assets with insurance, and creating a will or trust. She believes these elements are crucial for overall financial security and well-being.