To be considered, the final response should strictly adhere to all instructions.

The net worth required to be considered upper class rises sharply with age, and for those in their 60s, reaching the upper echelons of wealth demands a significantly larger portfolio than for younger individuals, according to recent analysis.

For Americans in their 60s aspiring to join the upper class, accumulating a net worth of at least $3.4 million is generally considered the threshold, though some analyses suggest an even higher figure may be necessary to truly feel affluent, challenging conventional benchmarks for retirement savings and financial security. This figure reflects not only accumulated savings and investments but also the increasing cost of living and healthcare, impacting retirement planning and lifestyle expectations. As individuals approach retirement, the definition of “rich” evolves, necessitating a substantial financial cushion to maintain a comfortable lifestyle and address potential unforeseen expenses.

The notion of being “rich” is subjective and often tied to personal financial goals and lifestyle aspirations. However, when examining the quantitative measures used to define wealth tiers, a clearer picture emerges of what it takes to be considered part of the upper class, especially during the retirement years. While some financial advisors propose a lower target, the general consensus points to a multi-million dollar net worth as a crucial milestone for those in their 60s aiming to achieve and maintain an upper-class lifestyle. This financial achievement allows for not only comfortable living but also the peace of mind that comes with financial stability and the ability to cover unexpected costs without jeopardizing long-term financial security.

The landscape of retirement has shifted dramatically, influenced by factors like increasing longevity, inflation, and evolving healthcare expenses. These elements have collectively pushed the bar higher for what it means to be financially secure in retirement, influencing how individuals plan for their later years. For those nearing or already in their 60s, the challenge is to accumulate and manage a portfolio large enough to provide a sustained income stream that matches their desired lifestyle. This necessitates not just substantial savings but also careful investment strategies, tax planning, and a realistic assessment of future expenses.

Accumulating a net worth of $3.4 million, or possibly more, involves strategic financial planning and consistent effort throughout one’s working life. It requires a combination of diligent saving habits, prudent investment choices, and, in some cases, the willingness to take calculated risks to grow wealth. The journey to reaching this level of affluence is unique for each individual, shaped by their income, spending habits, investment acumen, and unexpected life events. However, the underlying principles remain the same: save early, invest wisely, and manage debt effectively.

Furthermore, the perceived value of wealth is not solely defined by the numbers in a bank account. For many retirees, financial security is also about having the freedom to pursue their passions, spend time with loved ones, and contribute to their communities. This qualitative aspect of wealth adds another dimension to the conversation, suggesting that being “rich” is as much about experiences and relationships as it is about financial assets. Therefore, while the $3.4 million benchmark provides a tangible goal, it’s essential to remember that true wealth encompasses a broader range of factors that contribute to overall well-being.

The composition of net worth is another crucial element to consider. A significant portion of the $3.4 million should ideally be held in liquid assets that can be readily accessed in case of emergencies or unexpected expenses. This may include cash, stocks, bonds, and other investments that can be easily converted to cash. Conversely, illiquid assets, such as real estate or private equity, may provide long-term growth potential but may not be readily available for immediate needs. A balanced portfolio that combines both liquid and illiquid assets is often the most effective strategy for maximizing wealth and ensuring financial security in retirement.

Moreover, tax planning plays a significant role in preserving wealth and ensuring that it lasts throughout retirement. Understanding the tax implications of different investment vehicles, retirement accounts, and estate planning strategies is essential for minimizing tax liabilities and maximizing the after-tax value of assets. Working with a qualified tax advisor can help retirees navigate the complexities of the tax system and develop strategies to minimize their tax burden and protect their wealth.

In addition to financial assets, healthcare costs represent a substantial expense for retirees. As individuals age, their healthcare needs tend to increase, and the cost of medical care can quickly erode even the most substantial retirement savings. Planning for healthcare expenses is therefore a crucial aspect of retirement planning. This may involve purchasing supplemental health insurance, considering long-term care insurance, and budgeting for out-of-pocket medical expenses.

The concept of “upper class” is often associated with luxury and extravagance, but for many retirees, it simply means having the financial freedom to live comfortably and pursue their interests without worrying about running out of money. This may involve traveling, pursuing hobbies, spending time with family and friends, and contributing to charitable causes. Ultimately, the goal of accumulating wealth is to enhance one’s quality of life and provide a sense of security and peace of mind.

In conclusion, while the $3.4 million net worth threshold provides a useful benchmark for those in their 60s aspiring to join the upper class, it’s important to remember that wealth is a multifaceted concept that encompasses financial assets, personal relationships, and overall well-being. Strategic financial planning, diligent saving habits, and a focus on long-term financial security are essential for achieving and maintaining a comfortable lifestyle throughout retirement. Moreover, the definition of “rich” is ultimately subjective and depends on individual goals, values, and lifestyle aspirations.

Expanding on Key Aspects and Considerations

Defining Upper Class: The term “upper class” is often associated with wealth, power, and prestige, but its definition can be subjective and vary depending on socioeconomic context. Generally, the upper class represents the highest stratum of society in terms of income, wealth, and social status. Determining the precise financial threshold for belonging to the upper class is challenging, as it depends on factors such as location, cost of living, and lifestyle preferences.

Net Worth Calculation: Net worth is a measure of an individual’s or household’s financial position, calculated by subtracting total liabilities (debts) from total assets. Assets include items such as cash, investments, real estate, and personal property, while liabilities include debts such as mortgages, loans, and credit card balances. A positive net worth indicates that assets exceed liabilities, while a negative net worth indicates the opposite.

Factors Influencing Net Worth: Numerous factors can influence an individual’s or household’s net worth, including income, savings rate, investment returns, debt levels, and unexpected financial events. High-income earners who save a significant portion of their income and invest wisely are more likely to accumulate substantial net worth over time. Conversely, individuals with high debt levels or those who experience financial setbacks may struggle to build wealth.

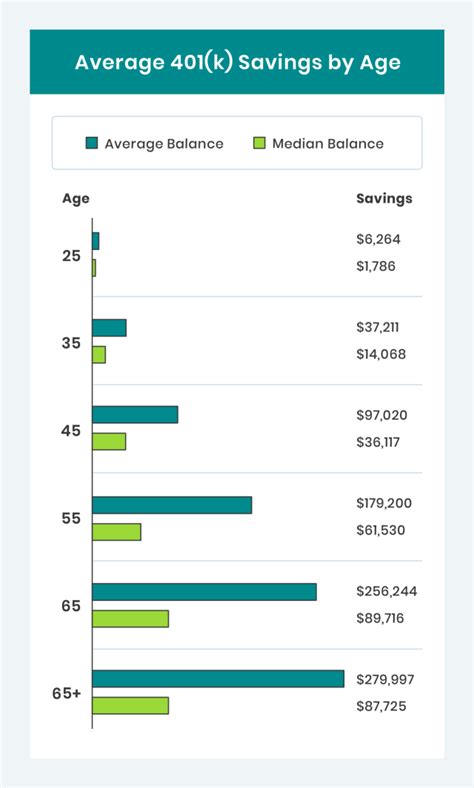

The Impact of Age: Age plays a significant role in determining the net worth required to be considered upper class. As individuals age, they typically have more time to accumulate wealth through savings, investments, and asset appreciation. Therefore, the net worth threshold for belonging to the upper class tends to increase with age. For those in their 60s, who are typically nearing or already in retirement, a higher net worth is generally required to maintain a comfortable lifestyle and cover potential healthcare expenses.

Geographic Variations: The cost of living varies significantly across different geographic regions, which can impact the net worth required to be considered upper class. In high-cost areas such as major metropolitan cities, a higher net worth may be necessary to maintain a comparable standard of living compared to lower-cost areas. Therefore, it’s essential to consider geographic location when assessing the financial threshold for belonging to the upper class.

Investment Strategies: Investment strategies play a crucial role in building and preserving wealth. Prudent investment choices can help individuals grow their assets over time and achieve their financial goals. Diversification, which involves spreading investments across different asset classes, is a key principle of sound investing. A well-diversified portfolio can help reduce risk and maximize potential returns.

Retirement Planning: Retirement planning is an essential aspect of financial planning, particularly for those nearing or already in their 60s. Adequate retirement savings are necessary to maintain a comfortable lifestyle and cover potential healthcare expenses during retirement. Individuals should consider factors such as their desired retirement age, estimated expenses, and investment returns when developing their retirement plan.

Healthcare Costs: Healthcare costs represent a significant expense for retirees. As individuals age, their healthcare needs tend to increase, and the cost of medical care can quickly erode even the most substantial retirement savings. Planning for healthcare expenses is therefore a crucial aspect of retirement planning. This may involve purchasing supplemental health insurance, considering long-term care insurance, and budgeting for out-of-pocket medical expenses.

Estate Planning: Estate planning involves arranging for the management and distribution of one’s assets after death. A well-designed estate plan can help minimize estate taxes, ensure that assets are distributed according to one’s wishes, and provide for the financial security of loved ones. Estate planning may involve creating a will, establishing trusts, and making arrangements for healthcare directives.

Beyond Monetary Wealth: While financial wealth is an important component of overall well-being, it’s essential to recognize that wealth encompasses more than just monetary assets. Personal relationships, health, happiness, and a sense of purpose also contribute to overall quality of life. Therefore, while accumulating financial wealth is a worthwhile goal, it’s important to prioritize other aspects of well-being as well.

The Role of Financial Advisors: Financial advisors can provide valuable guidance and support in helping individuals achieve their financial goals. A qualified financial advisor can help assess one’s financial situation, develop a comprehensive financial plan, and provide ongoing investment advice. Working with a financial advisor can help individuals make informed decisions about their finances and maximize their chances of achieving financial success.

Inflation and its Impact: Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. Inflation significantly impacts retirement planning because it erodes the value of savings over time. Retirees need to factor inflation into their financial projections to ensure that their savings will last throughout their retirement years. Failure to account for inflation can lead to a shortfall in retirement income and force retirees to make difficult choices about their lifestyle.

Social Security Benefits: Social Security benefits provide a crucial source of income for many retirees. The amount of Social Security benefits an individual receives depends on their earnings history and the age at which they begin claiming benefits. Individuals should carefully consider their options for claiming Social Security benefits to maximize their lifetime income.

Pension Plans: Pension plans provide a defined benefit to retirees based on their years of service and earnings history. However, traditional pension plans are becoming increasingly rare, with many employers shifting to defined contribution plans such as 401(k)s. Individuals who have access to a pension plan should carefully consider its benefits and how it fits into their overall retirement plan.

Alternative Income Streams: In addition to Social Security and pension benefits, retirees may consider alternative income streams to supplement their retirement income. These may include part-time work, rental income from real estate investments, or income from a business. Exploring alternative income streams can help retirees increase their financial security and maintain a comfortable lifestyle.

Downsizing and Lifestyle Adjustments: As individuals approach retirement, they may consider downsizing their home or making other lifestyle adjustments to reduce their expenses. Downsizing can free up capital that can be used to fund retirement, while other lifestyle adjustments can help retirees reduce their overall cost of living.

The Importance of Flexibility: Retirement planning should be flexible and adaptable to changing circumstances. Unexpected events such as healthcare emergencies or economic downturns can impact retirement plans. Therefore, it’s essential to have a contingency plan in place and be prepared to make adjustments as needed.

Legacy Planning and Philanthropy: As individuals accumulate wealth, they may consider legacy planning and philanthropy. Legacy planning involves making arrangements for the distribution of one’s assets to future generations, while philanthropy involves donating to charitable causes. Legacy planning and philanthropy can provide a sense of purpose and fulfillment in retirement.

Continuing Education and Skill Development: Continuing education and skill development can help retirees stay engaged and active during retirement. Learning new skills can open up opportunities for part-time work, volunteering, or pursuing hobbies. Continuing education can also help retirees stay mentally sharp and connected to their communities.

Maintaining Social Connections: Maintaining social connections is essential for overall well-being during retirement. Strong social connections can provide emotional support, reduce feelings of loneliness, and improve cognitive function. Retirees should make an effort to stay connected with friends, family, and community groups.

The Psychological Aspects of Wealth: Accumulating and managing wealth can have both positive and negative psychological effects. While wealth can provide a sense of security and freedom, it can also lead to stress, anxiety, and feelings of isolation. It’s essential to maintain a healthy perspective on wealth and prioritize relationships, health, and overall well-being.

Addressing Longevity Risk: Longevity risk refers to the risk of outliving one’s savings during retirement. As life expectancies increase, retirees need to plan for a longer retirement period. This may involve saving more, investing more aggressively, or considering strategies to generate income throughout retirement.

Reverse Mortgages: A reverse mortgage is a type of loan that allows homeowners aged 62 and older to borrow against the equity in their home without having to make monthly payments. Reverse mortgages can provide a source of income for retirees, but they also come with risks and costs that should be carefully considered.

Long-Term Care Insurance: Long-term care insurance helps cover the costs of long-term care services such as nursing home care, assisted living, and home healthcare. As individuals age, the likelihood of needing long-term care increases. Long-term care insurance can help protect against the financial burden of long-term care expenses.

The Impact of Unexpected Events: Unexpected events such as job loss, illness, or natural disasters can significantly impact retirement plans. It’s essential to have an emergency fund in place to cover unexpected expenses and to review insurance coverage regularly.

Building a Strong Financial Foundation: Building a strong financial foundation involves establishing good financial habits such as budgeting, saving, and managing debt. A strong financial foundation can help individuals achieve their financial goals and prepare for unexpected events.

Frequently Asked Questions (FAQ)

Q1: How is “upper class” defined in the context of this article?

A1: In this context, “upper class” refers to the highest socioeconomic stratum, defined primarily by net worth and the ability to maintain a comfortable and financially secure lifestyle, particularly during retirement. While the exact definition can be subjective, a net worth of at least $3.4 million for those in their 60s is generally considered a benchmark. The definition also incorporates the ability to afford luxuries and cover unexpected expenses without financial strain.

Q2: What constitutes “net worth,” and how is it calculated?

A2: Net worth is calculated by subtracting total liabilities (debts) from total assets. Assets include cash, investments (stocks, bonds, mutual funds), real estate, retirement accounts, and personal property. Liabilities encompass debts like mortgages, loans, credit card balances, and other outstanding obligations. The resulting figure provides a snapshot of an individual’s or household’s financial position.

Q3: Why is a higher net worth required to be considered upper class in your 60s compared to younger age groups?

A3: A higher net worth is needed in your 60s due to several factors: shorter time horizon to recover from financial setbacks, the need for a larger nest egg to fund retirement expenses (potentially for 20-30 years or more), increased healthcare costs, and the desire to maintain a comfortable lifestyle without relying on earned income. The accumulated wealth is expected to generate income and cover expenses throughout retirement.

Q4: Besides financial assets, what other factors contribute to a sense of wealth and well-being in retirement?

A4: Beyond financial assets, factors such as strong personal relationships, good health, a sense of purpose (through hobbies, volunteering, or part-time work), and the ability to pursue passions significantly contribute to a sense of wealth and well-being in retirement. These non-financial aspects can enhance overall quality of life and provide fulfillment beyond monetary wealth.

Q5: What are some key strategies for building and maintaining a substantial net worth for retirement?

A5: Key strategies include:

- Early and Consistent Saving: Start saving early in your career and make it a consistent habit.

- Prudent Investing: Invest wisely in a diversified portfolio that aligns with your risk tolerance and long-term goals.

- Debt Management: Avoid excessive debt and manage existing debt effectively.

- Tax Planning: Minimize tax liabilities through strategic tax planning.

- Healthcare Planning: Prepare for healthcare expenses by purchasing supplemental insurance or setting aside funds specifically for medical costs.

- Financial Advisor: Seek guidance from a qualified financial advisor to create and manage a personalized financial plan.

- Regular Review: Review and adjust your financial plan periodically to account for changes in circumstances and market conditions.

- Long-Term Perspective: Take a long-term perspective and remain disciplined in your investment approach.