Average 401(k) and IRA balances vary significantly by age, offering a snapshot of Americans’ retirement readiness and highlighting the challenges many face in accumulating sufficient savings. While some are on track, many lag behind recommended benchmarks, underscoring the need for proactive planning and consistent contributions throughout their working lives.

Retirement Savings: A Look at Average Balances

Fidelity Investments’ analysis of millions of 401(k) and IRA accounts reveals a wide range of retirement savings levels, reflecting diverse income levels, savings habits, and investment strategies. These averages provide a useful, albeit imperfect, benchmark for individuals assessing their own progress. However, experts caution against relying solely on averages, emphasizing the importance of personalized retirement plans tailored to individual circumstances.

As of the latest data, the average 401(k) balance across all age groups is approximately $118,600. However, this figure masks significant disparities among different age cohorts. Younger workers, naturally, have lower balances due to less time in the workforce and competing financial priorities. Conversely, older workers approaching retirement age typically have higher balances, reflecting decades of contributions and investment growth.

The average IRA balance also varies considerably. While the overall average is around $123,800, this number doesn’t tell the whole story. Factors such as contribution limits, investment choices, and rollover activity from employer-sponsored plans significantly influence individual balances.

Age-Specific Averages: A Detailed Breakdown

Examining average balances by age group offers a more nuanced understanding of retirement savings trends. While these figures are merely averages and do not represent individual circumstances, they provide valuable context for assessing retirement readiness.

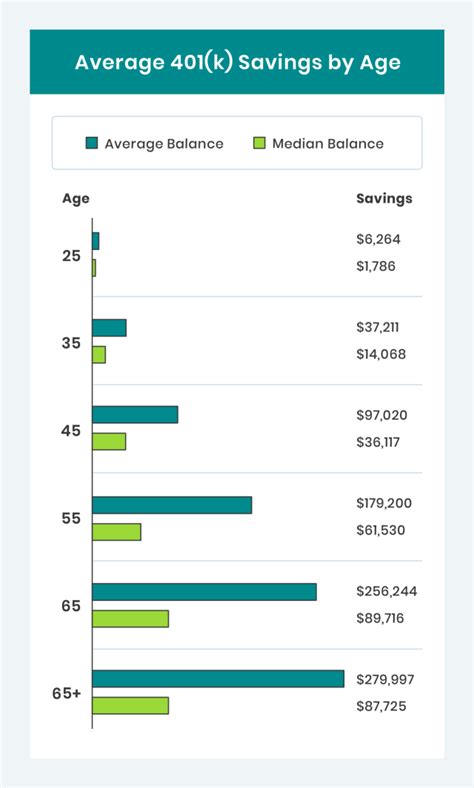

- 20s: Individuals in their 20s are just beginning their careers and retirement savings journeys. As such, average 401(k) balances in this age group are relatively low, typically ranging from $10,000 to $30,000. Those focused on aggressive repayment of student loan debt may have lower savings. IRA balances are similarly modest, often reflecting initial contributions and limited investment experience.

- 30s: As careers progress and incomes rise, individuals in their 30s tend to increase their retirement savings contributions. Average 401(k) balances in this age group range from $40,000 to $80,000. IRA balances also see a corresponding increase, reflecting higher contribution levels and the potential for investment growth. This is often a period where debt reduction competes with retirement savings goals.

- 40s: The 40s are often a crucial decade for retirement planning. Individuals in this age group typically have higher earning potential and are better positioned to make substantial contributions to their retirement accounts. Average 401(k) balances range from $100,000 to $250,000. IRA balances continue to grow, potentially surpassing $100,000 for those who have consistently contributed over time.

- 50s: Approaching retirement age, individuals in their 50s should have accumulated a significant portion of their retirement savings. Average 401(k) balances in this age group range from $250,000 to $500,000 or more. IRA balances are also typically substantial, reflecting decades of contributions and investment growth. The “catch-up” contribution provisions allow those over 50 to contribute more to their retirement accounts.

- 60s: Individuals in their 60s are nearing or already in retirement. Average 401(k) balances in this age group can range from $400,000 to $700,000 or higher, depending on factors such as income, savings habits, and investment performance. IRA balances are often at their peak, providing a significant source of retirement income.

Factors Influencing Retirement Savings

Numerous factors influence an individual’s retirement savings trajectory. Understanding these factors is crucial for developing an effective retirement plan and making informed financial decisions.

- Income: Income is a primary driver of retirement savings. Higher-income individuals typically have more discretionary income available to contribute to retirement accounts. As salaries increase over a worker’s career, so does the ability to save for retirement.

- Savings Rate: The savings rate, or the percentage of income contributed to retirement accounts, plays a significant role in accumulating wealth over time. A higher savings rate leads to faster growth in retirement balances. Experts often recommend saving at least 10-15% of one’s income for retirement, including any employer matching contributions.

- Investment Choices: Investment choices significantly impact the growth of retirement savings. A diversified portfolio that balances risk and return is essential for maximizing long-term growth potential. Investing in a mix of stocks, bonds, and other asset classes can help mitigate risk and enhance returns.

- Employer Matching Contributions: Employer matching contributions are a valuable benefit that can significantly boost retirement savings. Many employers offer to match a portion of employee contributions to 401(k) plans, effectively providing “free money” for retirement. Taking full advantage of employer matching contributions is a key strategy for maximizing retirement savings.

- Time Horizon: The time horizon, or the length of time until retirement, is a critical factor in determining investment strategy and savings goals. Younger workers with longer time horizons can typically afford to take on more risk in their investment portfolios, while older workers nearing retirement may prefer a more conservative approach.

- Financial Literacy: A strong understanding of personal finance principles is essential for making informed decisions about retirement savings. Financial literacy empowers individuals to budget effectively, manage debt, and make sound investment choices.

- Debt: High levels of debt can impede retirement savings. Prioritizing debt repayment, particularly high-interest debt, can free up more income for retirement contributions.

- Market Performance: Market performance significantly impacts the value of retirement investments. Bull markets can lead to substantial gains, while bear markets can erode savings. Diversification and a long-term investment perspective can help mitigate the impact of market volatility.

- Life Events: Major life events, such as marriage, divorce, childbirth, and job loss, can significantly impact retirement savings. These events often require adjustments to financial plans and savings strategies.

- Withdrawals: Withdrawing money from retirement accounts before retirement can significantly reduce long-term savings. Early withdrawals are typically subject to taxes and penalties, further diminishing their value.

The Importance of Early Planning and Consistent Contributions

Experts emphasize the importance of starting to save for retirement early and contributing consistently throughout one’s working life. The power of compounding allows investments to grow exponentially over time, making early savings particularly valuable. Even small contributions made early in one’s career can accumulate significantly over several decades.

Delaying retirement savings can make it more challenging to catch up later in life. As retirement approaches, individuals may need to make significantly larger contributions to reach their savings goals. Early planning and consistent contributions can help avoid this scenario and ensure a more secure retirement.

Addressing the Retirement Savings Gap

Many Americans face a retirement savings gap, meaning they are not on track to accumulate sufficient savings to maintain their current standard of living in retirement. Several factors contribute to this gap, including inadequate savings rates, insufficient investment returns, and unexpected expenses.

Addressing the retirement savings gap requires a multi-faceted approach. Individuals can take steps to increase their savings rates, improve their investment strategies, and manage their expenses effectively. Employers can play a role by offering robust retirement plans with employer matching contributions and financial education programs. Policymakers can also implement policies to encourage retirement savings, such as automatic enrollment in retirement plans and tax incentives for contributions.

Strategies for Enhancing Retirement Savings

Individuals can employ various strategies to enhance their retirement savings and improve their financial security in retirement.

- Increase Savings Rate: The most direct way to boost retirement savings is to increase the percentage of income contributed to retirement accounts. Even a small increase in the savings rate can make a significant difference over time.

- Take Advantage of Employer Matching Contributions: Maximizing employer matching contributions is a crucial strategy for maximizing retirement savings. Ensure you are contributing enough to your 401(k) to receive the full employer match.

- Automate Savings: Automating retirement savings can help ensure consistent contributions. Set up automatic transfers from your checking account to your retirement accounts each month.

- Review Investment Portfolio Regularly: Review your investment portfolio regularly to ensure it aligns with your risk tolerance and retirement goals. Consider rebalancing your portfolio periodically to maintain your desired asset allocation.

- Consider a Roth IRA or Roth 401(k): Roth accounts offer tax advantages that can be beneficial for some individuals. Contributions to Roth accounts are made with after-tax dollars, but withdrawals in retirement are tax-free.

- Delay Social Security Benefits: Delaying Social Security benefits can result in a higher monthly payment in retirement. For each year you delay claiming benefits beyond your full retirement age (up to age 70), your benefits will increase by a certain percentage.

- Work with a Financial Advisor: A financial advisor can provide personalized guidance on retirement planning and investment management. They can help you develop a retirement plan tailored to your specific circumstances and goals.

- Reduce Expenses: Cutting unnecessary expenses can free up more income for retirement savings. Review your budget and identify areas where you can reduce spending.

- Consider a Side Hustle: Earning extra income through a side hustle can provide additional funds for retirement savings. Consider pursuing a part-time job or freelance work to supplement your income.

- Stay Informed: Stay informed about retirement planning and investment strategies. Read articles, attend seminars, and consult with financial professionals to enhance your knowledge.

Retirement Planning Beyond Savings: Other Considerations

While accumulating sufficient savings is crucial for retirement security, other factors also play a significant role.

- Healthcare Costs: Healthcare costs are a significant expense in retirement. Plan for these costs by considering long-term care insurance and exploring Medicare options.

- Housing Costs: Housing costs can also be a significant expense in retirement. Consider downsizing or relocating to a more affordable area.

- Inflation: Inflation can erode the purchasing power of retirement savings over time. Factor inflation into your retirement planning and consider investing in assets that can keep pace with inflation.

- Longevity: People are living longer than ever before, so it’s essential to plan for a potentially long retirement. Estimate your life expectancy and plan accordingly.

- Taxes: Taxes can significantly impact retirement income. Understand the tax implications of different retirement accounts and plan accordingly.

- Estate Planning: Estate planning is essential for ensuring your assets are distributed according to your wishes after your death. Consult with an estate planning attorney to create a will or trust.

Conclusion

Retirement planning is a complex process that requires careful consideration of various factors. While average 401(k) and IRA balances provide a useful benchmark, they are not a substitute for personalized planning. Starting to save early, contributing consistently, and making informed investment decisions are crucial for achieving retirement security. By taking proactive steps to enhance their retirement savings, individuals can improve their financial well-being in retirement and enjoy a comfortable and fulfilling life. As the report stated, the key takeaway is that “consistent saving and investing habits” are critical for “long-term financial security”.

Frequently Asked Questions (FAQs)

-

What is the average 401(k) balance for someone in their 40s?

- According to Fidelity Investments data, the average 401(k) balance for individuals in their 40s ranges from $100,000 to $250,000. However, this is just an average, and individual balances may vary significantly based on income, savings habits, and investment choices.

-

How much should I be saving for retirement at age 30?

- Financial experts often recommend having approximately one year’s salary saved for retirement by age 30. While this is a general guideline, the actual amount needed will depend on individual circumstances, such as income, expenses, and retirement goals. Strive to save at least 10-15% of your income for retirement, including any employer matching contributions.

-

What are the benefits of a Roth IRA compared to a traditional IRA?

- Roth IRAs offer tax-free withdrawals in retirement, while traditional IRAs offer tax deductions on contributions. However, withdrawals from traditional IRAs are taxed in retirement. Roth IRAs may be more beneficial for individuals who expect to be in a higher tax bracket in retirement, while traditional IRAs may be more beneficial for those who expect to be in a lower tax bracket.

-

What is the “catch-up” contribution provision for retirement accounts?

- The “catch-up” contribution provision allows individuals age 50 and older to contribute more to their retirement accounts than younger workers. This provision is designed to help older workers catch up on their retirement savings as they approach retirement age. The specific amount allowed for catch-up contributions varies depending on the type of retirement account.

-

Should I work with a financial advisor to plan for retirement?

- Working with a financial advisor can be beneficial for many individuals, particularly those who are not comfortable managing their own finances or who need help developing a comprehensive retirement plan. A financial advisor can provide personalized guidance on retirement planning, investment management, and other financial matters. However, it’s essential to choose a qualified and trustworthy advisor who acts in your best interest.