Home sellers clinging to unrealistic price expectations are facing a harsh reality check, as evidenced by a viral social media post highlighting the disconnect between seller aspirations and current market conditions.

A scathing open letter addressed to homeowners with inflated asking prices is making waves online, serving as a stark warning that the pandemic-fueled housing boom is firmly in the rearview mirror. The post, which has resonated with frustrated buyers and real estate professionals alike, underscores the challenges sellers face in adjusting to a cooling market characterized by higher interest rates and increased inventory. “DEAR PRICE: Too High. Sincerely, Everyone,” the post emphatically states, encapsulating the prevailing sentiment among potential homebuyers.

The current housing market stands in stark contrast to the frenzied conditions of the recent past, where bidding wars and waived contingencies were commonplace. Now, buyers are exhibiting greater caution and exercising more leverage, demanding reasonable prices and thorough inspections. This shift has left many sellers, accustomed to the rapid appreciation of home values, struggling to recalibrate their expectations.

According to the original post, “’I’m seeing more and more homes sitting on the market for longer periods of time because the sellers are holding onto unrealistic price expectations.'” This resistance to accepting current market valuations is prolonging the sales process and contributing to a growing inventory of unsold homes.

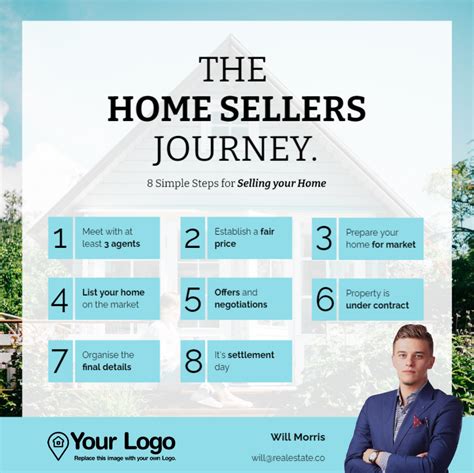

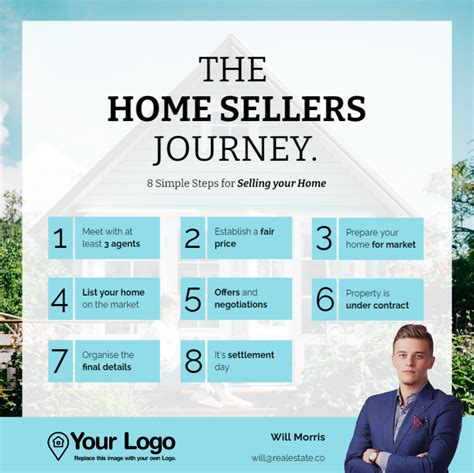

The viral post further emphasizes the importance of pricing a home competitively from the outset. Overpricing, the post warns, can lead to a property languishing on the market, ultimately forcing sellers to accept a lower price than they might have initially obtained had they priced realistically. The post suggests that sellers should consult with experienced real estate agents to determine a fair market value based on recent comparable sales and current market conditions.

The author of the viral post, believed to be a real estate professional, tapped into a collective frustration felt by many potential buyers. Sky-high prices, often justified by outdated comparisons to peak market conditions, are effectively pricing many families out of the market. The post’s success lies in its blunt and relatable message, highlighting the need for sellers to acknowledge the changed landscape and adjust their expectations accordingly.

This “wake-up call” extends beyond individual sellers and has broader implications for the housing market as a whole. As inventory continues to rise and sales volume declines, downward pressure on prices is likely to intensify. Sellers who remain intransigent on price risk missing the window of opportunity to sell their homes at a favorable price, potentially facing even steeper discounts in the future.

The situation is further complicated by rising interest rates, which have significantly increased the cost of borrowing for potential buyers. Higher mortgage rates translate into higher monthly payments, reducing affordability and further dampening demand. This, in turn, puts additional pressure on sellers to lower their prices in order to attract buyers.

The long-term consequences of clinging to unrealistic price expectations could include a slowdown in housing market activity, a decline in home values, and an increase in foreclosures. While a market correction is not necessarily a negative development – it can restore balance and improve affordability – it requires sellers to be realistic and responsive to changing market dynamics. The viral post serves as a timely reminder that the era of effortless profits in the housing market has come to an end, and that a more pragmatic approach is required for both buyers and sellers to navigate the current environment successfully.

Detailed Analysis of the Housing Market Shift

The real estate market’s pendulum swing from a seller’s paradise to a more balanced or even buyer-leaning environment is a complex phenomenon influenced by a confluence of factors. Understanding these factors is crucial for both sellers and buyers aiming to make informed decisions.

The End of Pandemic-Driven Frenzy: The COVID-19 pandemic triggered an unprecedented surge in housing demand, fueled by record-low interest rates, a shift towards remote work, and a desire for more space. This combination led to bidding wars, rapidly escalating prices, and a scarcity of available homes. However, as the pandemic waned and economic conditions evolved, this frenzied pace became unsustainable.

Rising Interest Rates: The Federal Reserve’s efforts to combat inflation by raising interest rates have had a significant impact on the housing market. Higher mortgage rates directly increase the cost of buying a home, reducing affordability for potential buyers. This has led to a decrease in demand and a cooling of the market. As interest rates continue to fluctuate, potential buyers are more cautious and price-sensitive.

Increased Inventory: As demand cools, the number of homes available for sale has been steadily increasing. This rise in inventory gives buyers more options and more leverage in negotiations. Sellers, who were once able to dictate terms, now face increased competition and are often forced to lower their prices to attract buyers. The level of inventory is a key indicator of the market’s health and its balance between buyers and sellers.

Shifting Buyer Sentiment: The psychology of the market has also shifted. Buyers, once eager to jump into bidding wars, are now more discerning and patient. They are taking their time to research properties, conduct thorough inspections, and negotiate favorable terms. This change in buyer sentiment reflects a broader awareness that the market is no longer characterized by rapid appreciation and that patience can be rewarded.

Impact on Sellers: For sellers, the transition to a more balanced market requires a significant adjustment in mindset. Those who cling to unrealistic price expectations are likely to experience longer listing times, fewer offers, and ultimately, the need to lower their prices. Pricing a home competitively from the outset is now more crucial than ever.

The Role of Real Estate Professionals: Experienced real estate agents play a vital role in helping sellers navigate the changing market. They can provide accurate market analysis, advise on pricing strategies, and help sellers understand the factors that influence buyer behavior. Agents can also help sellers prepare their homes for sale, highlighting their strengths and addressing any potential concerns.

Long-Term Implications: The current market correction is likely to have long-term implications for the housing market. While it may lead to a temporary slowdown in activity and a decline in home values, it can also create a more sustainable and balanced market in the long run. A more affordable housing market can benefit both buyers and sellers, fostering greater economic stability and opportunity.

The Importance of Realistic Expectations

The viral post serves as a potent reminder of the importance of setting realistic expectations in the current housing market. For sellers, this means understanding that the days of easy profits are over and that a more strategic approach is required.

Understanding Market Data: Sellers need to rely on current market data, rather than past performance, to determine a fair listing price. This includes analyzing recent comparable sales, tracking inventory levels, and monitoring interest rate trends.

Seeking Professional Advice: Consulting with an experienced real estate agent is essential. Agents can provide valuable insights into the local market and help sellers develop a pricing strategy that is both realistic and competitive.

Preparing the Home for Sale: Making necessary repairs and improvements can enhance a home’s appeal to potential buyers. This may include updating kitchens and bathrooms, painting walls, and improving curb appeal. A well-maintained home is more likely to attract buyers and command a higher price.

Being Flexible and Responsive: Sellers need to be prepared to adjust their expectations and pricing strategy based on market feedback. If a home is not generating interest, it may be necessary to lower the price or make other concessions to attract buyers.

Avoiding Overpricing: Overpricing a home is one of the biggest mistakes sellers can make. It can deter potential buyers, lead to longer listing times, and ultimately result in a lower sales price. It’s far better to price a home competitively from the outset and generate interest and multiple offers.

The Psychology of Pricing: Pricing a home is not just about numbers; it’s also about psychology. Buyers are often drawn to homes that are perceived as a good value. Pricing a home slightly below market value can create a sense of urgency and generate more interest.

The Impact of Interest Rates on Affordability

Rising interest rates have a direct and significant impact on housing affordability, making it more challenging for potential buyers to enter the market. Understanding this impact is crucial for both buyers and sellers.

How Interest Rates Affect Mortgage Payments: Higher interest rates translate directly into higher monthly mortgage payments. Even a small increase in interest rates can add hundreds of dollars to a monthly payment, significantly reducing affordability.

The Impact on Borrowing Power: As interest rates rise, buyers’ borrowing power decreases. They may be able to afford a smaller loan amount, limiting their options in terms of the type and size of home they can purchase.

The Relationship Between Interest Rates and Demand: Higher interest rates tend to dampen demand for housing, as fewer people are able to afford to buy a home. This decrease in demand puts downward pressure on prices.

The Long-Term Cost of Homeownership: Interest rates have a significant impact on the total cost of homeownership over the life of a mortgage. Even a small difference in interest rates can result in tens of thousands of dollars in additional interest paid.

Strategies for Buyers in a Rising Rate Environment: Buyers facing rising interest rates may need to adjust their strategies. This may include considering smaller homes, looking in more affordable areas, or waiting for interest rates to stabilize.

Strategies for Sellers in a Rising Rate Environment: Sellers in a rising rate environment need to be even more mindful of pricing their homes competitively. They may also need to offer incentives, such as paying closing costs or providing a home warranty, to attract buyers.

The Importance of Financial Planning: Rising interest rates highlight the importance of careful financial planning for both buyers and sellers. Buyers should work with a financial advisor to determine how much they can afford to spend on a home, while sellers should carefully analyze their financial situation before making a decision to sell.

The Role of Market Correction

The current shift in the housing market can be viewed as a market correction, a process that restores balance and improves affordability. While market corrections can be unsettling, they are a normal part of the economic cycle.

What is a Market Correction? A market correction is a decline in asset prices, typically occurring after a period of rapid appreciation. In the housing market, a correction can involve a decrease in home values and a slowdown in sales activity.

The Causes of Market Corrections: Market corrections are often triggered by changes in economic conditions, such as rising interest rates, inflation, or a slowdown in economic growth. They can also be caused by speculative bubbles or unsustainable levels of demand.

The Benefits of Market Corrections: Market corrections can have several benefits. They can restore affordability, reduce speculation, and create a more sustainable housing market. They can also provide opportunities for first-time homebuyers to enter the market.

The Risks of Market Corrections: Market corrections can also have risks. They can lead to a decline in home values, which can negatively impact homeowners’ equity. They can also trigger a slowdown in economic activity.

Managing the Risks of Market Corrections: Homeowners can manage the risks of market corrections by avoiding overleveraging themselves, maintaining a diversified investment portfolio, and staying informed about market conditions.

The Long-Term Outlook: While market corrections can be painful in the short term, they are often followed by periods of renewed growth. The long-term outlook for the housing market remains positive, as demand for housing is expected to continue to grow in the coming years.

The Impact on First-Time Homebuyers

The changing housing market presents both challenges and opportunities for first-time homebuyers. While rising interest rates can make it more difficult to afford a home, declining prices and increased inventory can create more favorable conditions.

The Challenges for First-Time Homebuyers: Rising interest rates and high home prices can make it challenging for first-time homebuyers to enter the market. They may need to save for a larger down payment, qualify for a smaller loan, or consider smaller homes in more affordable areas.

The Opportunities for First-Time Homebuyers: Declining prices and increased inventory can create opportunities for first-time homebuyers. They may be able to find homes at more affordable prices, negotiate better terms, and take their time to find the right property.

Strategies for First-Time Homebuyers: First-time homebuyers can improve their chances of success by carefully planning their finances, getting pre-approved for a mortgage, and working with an experienced real estate agent.

The Importance of Education: First-time homebuyers should educate themselves about the home buying process, including the different types of mortgages, the importance of inspections, and the negotiation process.

Utilizing Government Programs: There are many government programs available to help first-time homebuyers, such as down payment assistance programs, tax credits, and low-interest mortgages.

The Long-Term Benefits of Homeownership: Despite the challenges, homeownership remains a valuable long-term investment. It can provide stability, build equity, and offer a sense of community.

Conclusion: Navigating the New Housing Landscape

The housing market is undergoing a significant transformation, requiring both buyers and sellers to adapt to the new realities. The era of effortless profits and rapidly escalating prices is over, and a more pragmatic approach is needed. Sellers must adjust their price expectations, while buyers must be patient and strategic.

By understanding the factors that are influencing the market, seeking professional advice, and being prepared to adjust their strategies, both buyers and sellers can successfully navigate the new housing landscape and achieve their real estate goals. The viral post serves as a valuable reminder that realistic expectations, informed decision-making, and a willingness to adapt are essential for success in the current market environment. Frequently Asked Questions (FAQ)

1. Why are home prices not as high as they were during the peak of the pandemic?

The primary reason for the shift is the increase in mortgage interest rates. During the pandemic, rates were at historic lows, fueling demand and pushing prices up. As the Federal Reserve has raised rates to combat inflation, borrowing costs have increased significantly, reducing affordability for buyers. This, in turn, has cooled demand and led to price stabilization or even declines in some areas. Other factors include increased housing inventory, as more homes are available for sale, and a general shift in buyer sentiment towards more caution and less willingness to engage in bidding wars. The era of remote work also played a role, but as companies bring employees back to the office, that effect has diminished.

2. What should sellers do if their home is not selling at the price they want?

The first step is to have an honest conversation with their real estate agent. The agent should provide updated market analysis, including recent comparable sales, to determine if the asking price is truly aligned with current market values. Sellers should also consider the condition of their home and make necessary repairs or improvements to enhance its appeal. If the price is indeed too high, a price reduction is often necessary. Sellers should also be flexible and consider offering incentives, such as covering closing costs or providing a home warranty, to attract buyers. Ultimately, it’s a balance between getting a fair price and being realistic about what the market will bear. Ignoring market feedback and clinging to an unrealistic price will only prolong the selling process and potentially lead to a lower sales price in the long run.

3. How do rising interest rates affect first-time homebuyers?

Rising interest rates directly impact the affordability of a home for first-time homebuyers. Higher rates mean higher monthly mortgage payments, reducing the amount they can afford to borrow. This can force them to consider smaller homes, look in less expensive areas, or delay their purchase altogether. It also means they need to save for a larger down payment to offset the increased cost of borrowing. However, a cooling market can also present opportunities. As prices stabilize or even decline, and as inventory increases, first-time homebuyers may find more options and less competition than they did during the peak of the pandemic. They should also explore first-time homebuyer programs offered by government agencies or lenders, which can provide down payment assistance or lower interest rates. Careful budgeting and financial planning are essential for navigating a rising rate environment.

4. Is the housing market going to crash?

While a significant market correction is underway in many areas, a full-blown crash similar to the 2008 financial crisis is unlikely. The underlying factors are different. In 2008, the crisis was fueled by subprime mortgages and widespread lending practices that were not sustainable. Today, lending standards are generally tighter, and borrowers are more qualified. While home prices may decline further in some areas, a sudden and catastrophic collapse is not the most probable scenario. Instead, a gradual adjustment towards a more balanced market is more likely. Factors to monitor include interest rate trends, economic growth, and housing inventory levels. A recession could exacerbate the downturn, but even in that scenario, the impact is likely to be less severe than in 2008.

5. What are the long-term implications of the current housing market correction?

The long-term implications of the current housing market correction are multifaceted. A more balanced market, characterized by reasonable prices and increased affordability, can ultimately be beneficial for the overall economy. It can encourage sustainable homeownership and reduce speculative investment. It may also lead to a shift in housing preferences, with more emphasis on affordability and functionality. For homeowners, it means managing expectations and focusing on long-term value rather than short-term gains. For renters, it may present opportunities to transition into homeownership as prices become more accessible. The correction could also lead to increased innovation in the housing industry, with a focus on developing more affordable and sustainable housing solutions. Overall, while the correction may present challenges in the short term, it can pave the way for a more stable and equitable housing market in the long run.