For those in their 60s, a net worth of $3.4 million places you in the upper class, according to recent data analyzing wealth distribution in the United States. This figure, considerably higher than the median net worth for this age group, highlights the significant wealth disparities and financial benchmarks associated with upper-class status.

Defining Upper Class Wealth in Your 60s

The threshold for being considered upper class isn’t a fixed number; instead, it’s a relative measure based on the distribution of wealth within a population. Recent analysis, drawing from sources such as the Survey of Consumer Finances and wealth distribution models, suggests that to be in the top 10% of wealth holders, individuals in their 60s need a net worth of approximately $3.4 million. This figure encompasses all assets, including real estate, investments, retirement accounts, and other valuable possessions, minus liabilities such as mortgages, loans, and other debts.

“The upper class is often defined as the top 10% of wealth holders. Reaching this level requires substantial financial planning, investment acumen, and, often, a significant period of wealth accumulation,” explains a financial analyst familiar with wealth distribution trends. This definition emphasizes that merely having a high income is not enough; true upper-class status is determined by the total value of accumulated assets.

Median vs. Upper-Class Net Worth

The stark contrast between the median net worth and the upper-class threshold illustrates the wealth inequality prevalent in the United States. While $3.4 million is the benchmark for the upper class, the median net worth for households headed by someone in their 60s is significantly lower. According to the Federal Reserve’s Survey of Consumer Finances, the median net worth for this demographic is closer to several hundred thousand dollars, a fraction of what’s required to be in the top 10%.

This disparity highlights that most Americans in their 60s are far from reaching upper-class status. Many are still working to secure their retirement, pay off debts, and manage daily expenses. The data underscores the challenges faced by middle- and lower-income households in accumulating substantial wealth.

Factors Contributing to Wealth Accumulation

Several factors influence the ability to accumulate a net worth of $3.4 million by your 60s. These include:

- Income: Higher-income individuals typically have more opportunities to save and invest.

- Education: Advanced education often leads to higher earning potential and better financial literacy.

- Investment Strategy: Prudent investment decisions, such as diversifying investments and taking advantage of compound interest, can significantly boost wealth accumulation.

- Homeownership: Owning real estate, particularly in appreciating markets, can contribute substantially to net worth.

- Inheritance: Inherited wealth can provide a significant head start in accumulating assets.

- Savings Habits: Consistent saving and budgeting habits are crucial for building wealth over time.

- Career Choices: Certain professions offer higher earning potential and opportunities for advancement.

- Market Conditions: Economic conditions and market performance can impact investment returns and asset values.

“Wealth accumulation is a multifaceted process that requires a combination of favorable circumstances, disciplined financial habits, and strategic decision-making,” notes a certified financial planner. “It’s not solely about how much you earn but also about how well you manage and grow your assets.”

Geographic Variations in Wealth

The cost of living and economic conditions vary significantly across different regions of the United States, which can influence the net worth required to be considered upper class. In high-cost-of-living areas, such as major metropolitan cities, a net worth of $3.4 million might provide a comfortable lifestyle but not necessarily an extravagant one. Conversely, in lower-cost-of-living areas, the same net worth could provide a significantly higher standard of living.

Real estate values, in particular, play a significant role in determining net worth. Homeowners in expensive markets, such as California and New York, may have substantially higher net worths due to the appreciation of their properties, even if their incomes are not significantly higher than those in other regions.

The Role of Retirement Planning

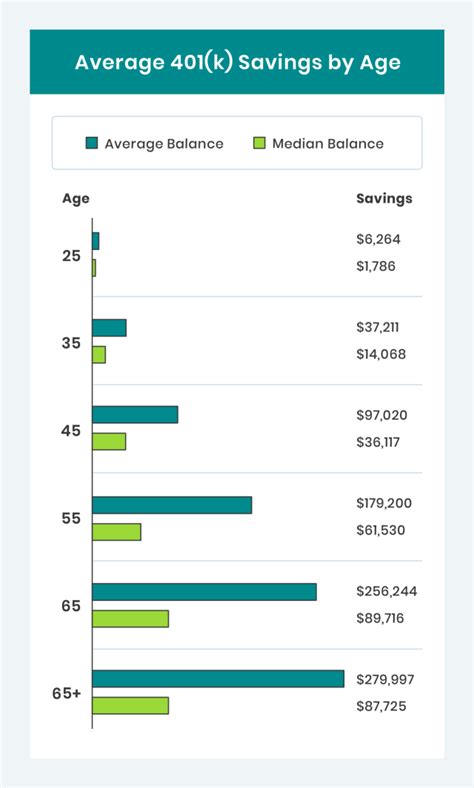

Retirement planning is a critical component of wealth accumulation, especially as individuals approach their 60s. A well-funded retirement account can significantly contribute to overall net worth and provide financial security during retirement years. Factors such as the age at which retirement planning begins, contribution levels, and investment choices can all impact the size of retirement savings.

Many financial advisors recommend starting retirement planning as early as possible and contributing consistently to retirement accounts, such as 401(k)s and IRAs. Taking advantage of employer-matching contributions and tax-advantaged savings plans can also help maximize retirement savings.

Impact of Economic Events

Economic events, such as recessions, market crashes, and inflation, can have a significant impact on wealth accumulation. During economic downturns, asset values may decline, leading to a decrease in net worth. Conversely, during periods of economic growth, asset values may increase, boosting net worth.

The COVID-19 pandemic, for example, had a mixed impact on wealth accumulation. While some individuals experienced financial hardship due to job losses and business closures, others saw their net worth increase due to rising stock prices and real estate values. Understanding how economic events can impact wealth and adjusting investment strategies accordingly is crucial for long-term financial success.

Lifestyle Considerations

While a net worth of $3.4 million may qualify individuals in their 60s as upper class, it’s important to consider lifestyle expectations. The level of comfort and financial security provided by this net worth will depend on factors such as spending habits, healthcare costs, travel plans, and philanthropic activities.

Some individuals may choose to live frugally and prioritize saving and investing, while others may prefer to spend more on leisure and luxury goods. The key is to align spending with financial goals and ensure that wealth is used in a way that provides both current enjoyment and long-term security.

Wealth Management Strategies

Effective wealth management strategies are essential for preserving and growing a net worth of $3.4 million. These strategies may include:

- Diversification: Spreading investments across different asset classes to reduce risk.

- Asset Allocation: Allocating investments based on risk tolerance and financial goals.

- Tax Planning: Minimizing tax liabilities through strategic investment and estate planning.

- Estate Planning: Creating a plan for the distribution of assets after death.

- Insurance Planning: Protecting assets from unexpected events through insurance coverage.

- Philanthropic Planning: Incorporating charitable giving into wealth management strategies.

“Working with a qualified financial advisor can help individuals develop and implement wealth management strategies that are tailored to their specific needs and goals,” advises a wealth management expert. “A financial advisor can provide guidance on investment decisions, tax planning, and estate planning, helping clients make the most of their wealth.”

The Psychological Impact of Wealth

Accumulating significant wealth can have both positive and negative psychological impacts. On the positive side, wealth can provide a sense of security, freedom, and accomplishment. It can also enable individuals to pursue their passions, support their families, and contribute to society.

However, wealth can also lead to stress, anxiety, and feelings of isolation. Managing a large net worth can be complex and time-consuming, and wealthy individuals may face challenges such as privacy concerns, security threats, and strained relationships. It’s important to maintain a healthy perspective on wealth and prioritize personal well-being.

The Future of Wealth Accumulation

The future of wealth accumulation is likely to be shaped by factors such as technological advancements, demographic shifts, and economic policies. Technological innovations, such as artificial intelligence and automation, could lead to increased productivity and higher incomes for some, while also displacing workers in certain industries.

Demographic trends, such as aging populations and increasing longevity, could impact retirement savings and healthcare costs. Economic policies, such as tax reforms and social welfare programs, could influence wealth distribution and opportunities for wealth accumulation.

The American Dream and Wealth

The concept of the American Dream, which traditionally involved upward mobility and financial success through hard work and determination, has evolved over time. While the American Dream remains a powerful aspiration for many, the reality is that wealth accumulation is becoming increasingly challenging for many Americans due to factors such as rising costs of living, stagnant wages, and increasing income inequality.

Despite these challenges, the pursuit of wealth remains a significant motivator for many individuals and families. Understanding the factors that contribute to wealth accumulation and adopting effective financial strategies can help individuals increase their chances of achieving their financial goals.

Wealth and Happiness

While wealth can provide financial security and opportunities, it’s important to recognize that it is not a guarantee of happiness. Studies have shown that there is a correlation between wealth and happiness, but the relationship is complex and influenced by factors such as social connections, purpose in life, and gratitude.

Many wealthy individuals find that true happiness comes from meaningful relationships, fulfilling work, and contributing to the well-being of others. It’s important to prioritize these non-material aspects of life and use wealth in a way that enhances personal fulfillment and makes a positive impact on the world.

The Importance of Financial Literacy

Financial literacy is essential for making informed financial decisions and building wealth. Understanding concepts such as budgeting, saving, investing, and debt management can empower individuals to take control of their finances and achieve their financial goals.

Financial literacy programs and resources are available through various organizations, including schools, community centers, and financial institutions. Taking the time to educate oneself about financial matters can have a significant impact on long-term financial success.

Conclusion

Achieving a net worth of $3.4 million by your 60s places you in the upper class, but it’s a milestone that requires careful planning, disciplined saving, and strategic investment. While this level of wealth provides financial security and opportunities, it’s important to remember that wealth is just one aspect of a fulfilling life. Focusing on personal well-being, meaningful relationships, and contributing to society can help ensure that wealth is used in a way that enhances overall happiness and quality of life. The journey to accumulating wealth is multifaceted, requiring not just high income but also astute management, strategic investment, and a bit of luck along the way.

Frequently Asked Questions (FAQ)

-

What net worth is considered upper class in the United States for people in their 60s?

According to recent analysis, a net worth of approximately $3.4 million is generally considered to place individuals in their 60s in the upper class, representing the top 10% of wealth holders. This figure encompasses all assets minus liabilities.

-

How does the median net worth for people in their 60s compare to the upper-class threshold?

The median net worth for households headed by someone in their 60s is significantly lower than the $3.4 million upper-class threshold. The median is closer to several hundred thousand dollars, highlighting the wealth disparity in this age group.

-

What factors contribute to the ability to accumulate a net worth of $3.4 million by your 60s?

Several factors play a role, including higher income, advanced education, prudent investment strategies, homeownership, inheritance, consistent savings habits, strategic career choices, and favorable market conditions. A combination of these factors increases the likelihood of substantial wealth accumulation.

-

How can retirement planning impact overall net worth for individuals in their 60s?

Retirement planning is critical. A well-funded retirement account significantly contributes to overall net worth and provides financial security during retirement. Starting early, consistent contributions, and smart investment choices can maximize retirement savings.

-

What are some effective wealth management strategies for preserving and growing a net worth of $3.4 million?

Effective strategies include diversification, strategic asset allocation, tax planning, comprehensive estate planning, insurance planning, and thoughtful philanthropic planning. Consulting with a qualified financial advisor can provide tailored guidance for these strategies.

Expanded Analysis and Context

Delving deeper into the factors that contribute to wealth accumulation reveals a complex interplay of socioeconomic elements and personal financial decisions. While a high income certainly provides a foundation for saving and investing, it’s not the sole determinant of reaching upper-class status. A person earning a substantial salary but burdened with significant debt or poor spending habits may struggle to accumulate wealth compared to someone with a more moderate income who consistently saves and invests wisely.

The Role of Education and Career Trajectory: Education levels directly correlate with earning potential, as higher education often unlocks access to higher-paying jobs and more specialized skills. Those with advanced degrees or specialized certifications are statistically more likely to command higher salaries throughout their careers, providing them with more disposable income to allocate toward savings and investments. Moreover, certain career paths naturally lend themselves to wealth accumulation. Careers in finance, technology, and entrepreneurship, for instance, often offer opportunities for high earnings and equity ownership, which can significantly boost net worth over time.

The Power of Compounding and Long-Term Investing: Time is a crucial element in wealth accumulation, particularly when it comes to the power of compounding. Starting to save and invest early in life allows individuals to take advantage of the snowball effect of compound interest, where earnings generate further earnings over time. Even relatively small contributions, when consistently made over several decades, can grow into substantial sums. Diversifying investments across different asset classes, such as stocks, bonds, and real estate, can further enhance returns and mitigate risk. A well-diversified portfolio, strategically managed, can weather market fluctuations and generate long-term growth.

Homeownership as a Wealth-Building Tool: Homeownership has long been considered a cornerstone of the American Dream and a significant driver of wealth accumulation. Owning a home provides stability, a sense of security, and the potential for long-term appreciation in value. As mortgage payments build equity over time, homeowners accumulate wealth in the form of their home’s value. Real estate can also serve as a hedge against inflation, as property values tend to rise along with the general price level. However, it’s important to note that homeownership also comes with responsibilities, such as property taxes, maintenance costs, and insurance, which can impact overall finances.

The Impact of Inheritance and Intergenerational Wealth Transfer: Inherited wealth can provide a significant head start in accumulating assets, particularly for those who receive substantial inheritances. Intergenerational wealth transfer, the passing down of assets from one generation to the next, plays a significant role in perpetuating wealth disparities. Individuals who inherit assets such as real estate, stocks, or businesses are often able to build upon that foundation and further increase their net worth. However, it’s important to recognize that inheritance is not the only path to wealth accumulation. Many individuals build their wealth through hard work, dedication, and smart financial decisions, regardless of their family background.

Navigating the Challenges of Inflation and Economic Volatility: Economic events, such as inflation and market volatility, can pose significant challenges to wealth accumulation. Inflation erodes the purchasing power of money, making it more expensive to buy goods and services. High inflation can reduce the real value of savings and investments, making it more difficult to reach financial goals. Market volatility, characterized by sharp fluctuations in stock prices, can also impact investment returns and lead to anxiety among investors. To mitigate these challenges, it’s important to diversify investments, stay informed about economic trends, and consult with a financial advisor to adjust investment strategies as needed.

The Role of Financial Literacy and Planning: Financial literacy, the ability to understand and effectively manage financial matters, is essential for building wealth. Individuals who are financially literate are better equipped to make informed decisions about budgeting, saving, investing, and debt management. Financial planning, the process of setting financial goals and developing strategies to achieve them, is also crucial. A comprehensive financial plan can help individuals stay on track, prioritize their spending, and make the most of their financial resources. Financial planning can also help individuals prepare for unexpected events, such as job loss or illness, and ensure that they have a safety net in place.

The Importance of Adaptability and Resilience: The path to wealth accumulation is rarely linear, and individuals may encounter setbacks along the way. Economic downturns, job losses, or unexpected expenses can all impact financial progress. Adaptability and resilience are key qualities for navigating these challenges. The ability to adjust financial strategies in response to changing circumstances, learn from mistakes, and persevere through difficult times can make a significant difference in long-term financial success. It’s also important to maintain a positive attitude and a long-term perspective, focusing on the big picture rather than getting discouraged by short-term setbacks.

The Ethical Considerations of Wealth Accumulation: As individuals accumulate wealth, it’s important to consider the ethical implications of their financial decisions. Wealth can be used for good or for ill, and it’s up to individuals to make choices that align with their values and contribute to the well-being of society. Philanthropy, charitable giving, and social impact investing are all ways that wealthy individuals can use their resources to make a positive difference in the world. It’s also important to be mindful of the potential for wealth to exacerbate inequality and to advocate for policies that promote economic justice and opportunity for all.

The Psychological Dimensions of Wealth: Accumulating wealth can have a profound impact on an individual’s psychological well-being. While wealth can provide a sense of security and freedom, it can also lead to stress, anxiety, and feelings of isolation. Managing a large net worth can be complex and time-consuming, and wealthy individuals may face challenges such as privacy concerns, security threats, and strained relationships. It’s important to maintain a healthy perspective on wealth and to prioritize personal well-being, meaningful relationships, and a sense of purpose in life.

Wealth Beyond Monetary Value: While this discussion focuses on net worth as a measure of wealth, it’s important to remember that wealth encompasses more than just monetary value. True wealth includes intangible assets such as health, relationships, knowledge, and experiences. Prioritizing these non-material aspects of life can lead to greater happiness and fulfillment, regardless of financial status.

In conclusion, reaching upper-class status, defined by a net worth of $3.4 million for those in their 60s, is a significant achievement that requires a combination of favorable circumstances, disciplined financial habits, and strategic decision-making. However, wealth is just one aspect of a fulfilling life, and it’s important to maintain a balanced perspective and prioritize personal well-being, meaningful relationships, and a sense of purpose. The journey to accumulating wealth is a long and complex one, requiring adaptability, resilience, and a commitment to ethical and responsible financial practices.